Digital Zeitgeist – What Exactly Are AT1 Bank Bonds And How Come Credit Suisse’s Were Completely Wiped Out

The Global Financial System is Under Strain Because of a Conflict Over Who Should Suffer Losses First in The Event That a Bank Fails

After the takeover of Credit Suisse by its larger rival UBS, which was brokered by the Swiss government, the global banking system is under renewed pressure because the deal wiped out the investment of bondholders who owned approximately $17 billion (£14 billion) of risky Credit Suisse debt.

What exactly has taken place?

The most recent worries are centred on a type of bank debt that was introduced after the financial crisis of 2008. This debt had been designed to increase banks’ safety buffers while tackling the “too big to fail” risk that they might require government support in a crisis. However, it appears that this debt may not be working as intended.

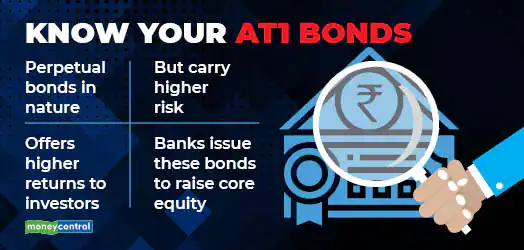

The bonds, which are meant to turn into equity (stock) in the event that a lender has financial difficulties, are referred to as additional tier 1 (AT1) bank debt.

The Swiss Financial Market Supervisory Authority (Finma) said that the purchase of Credit Suisse would result in a “complete writedown” of the value of all of the bank’s AT1 notes. This indicates that the bondholders would lose their whole investment as a result of the takeover.

This has caused the markets to become unsettled and has spurred a sell-off in other bank debt, as investors hurry to analyse if the same may happen for their holdings of AT1 debt in other banks, in a market that is worth more than $275 billion.

What is AT1 bank debt?

Banks are subject to stringent regulations as a result of the crucial role that they play as the suppliers of financing to millions of individuals and companies. These regulations include requirements about the amount of money that banks should keep aside to absorb potential losses.

In order to accomplish this, financial institutions keep a certain amount of capital on hand, which essentially refers to the money that is raised from shareholders and other investors, in addition to any profit that is retained. This capital is intended to act as a shock absorber in times of extreme stress.

Banks are required to maintain a number of distinct levels of capital, each of which is divided into tiers (much like a wedding cake), as a result of the laws that have been tightened after the 2008 financial crisis.

Common equity tier 1 capital is at the very top of the capital structure. It is the major source of financing for banks and is comprised of shareholders’ equity as well as retained profits.

After that comes AT1 capital, which is often made up of hybrid bonds. This is the next tier below. AT1 bonds are a form of debt that is issued by a bank and have the ability to be converted into equity if the bank’s capital levels fall below the criteria. These bonds are also frequently referred to as contingent convertible bonds, or CoCos. This contributes to the reduction of debts while also providing a boost to the bank’s capitalisation.

Tier 2 capital is the next layer of capital, and it might comprise subordinated debt, which are bonds that rank lower than senior debt and ordinary depositors.

Where did the issues at Credit Suisse originate from?

The major disagreement around the purchase of Credit Suisse centres on hierarchy, namely the question of who should suffer losses first when a bank is having financial difficulties. When a bank gets into financial problems, investors who purchased risky AT1 bonds should, on the one hand, anticipate suffering financial losses.

However, there are questions because Credit Suisse’s shareholders will not be wiped out completely but are set to be compensated in the emergency takeover with UBS shares worth the equivalent of Sfr 0.76 (£0.67) a share.

In the event that a company declares bankruptcy, the order of priority for creditors places bondholders ahead of shareholders in terms of any recovery that may be paid out. Notwithstanding the fact that they anticipated placing lower on the priority list than traditional bondholders, owners of AT1 bonds believed that they would still position higher than equity investors.

What happens next?

Documentation pertaining to bonds issued by Credit Suisse demonstrates that Swiss authorities have the authority to subvert the conventional order of things. Investors continue to be concerned about the possibility of a precedent being established, which would result in an increase in the cost of AT1 debt in the future.

“There will need to be further premium for those securities, at least in the current environment,” said Jerry del Missier, a former chief operating officer of Barclays who is now chief investment officer at Copper Street Capital.

“The message has clearly been sent that if a bank appears to be in trouble – and the definition of trouble now includes ‘loss of confidence’ in addition to solvency and liquidity considerations – AT1 holders will immediately price in a high probability of resolution.”

Attempting to calm the market rout on Monday, other European regulators issued statements saying that owners of AT1 debt would only experience losses after shareholders have been wiped out – unlike what happened at Credit Suisse.

Both the European Central Bank and the European Banking Authority have said that equity instruments would be the first to absorb losses, and that AT1 loans will not be forced to be written off until after all equity instruments have been exhausted. “This approach has been consistently applied in past cases and will continue to guide the actions of the SRB and ECB banking supervision in crisis interventions.”

According to the Bank of England, AT1 bonds are ranked higher than the highest tier of equity capital. Also, the Bank of England said that holders of such instruments should anticipate being exposed to losses in resolution or bankruptcy in the order of their positions in this hierarchy.

online sources: theguardian.com, finma.ch, cb.europa.eu, eba.europa.eu, bankofengland.co.uk