Digital Zeitgeist – Banking Bedlam – How Fearful Should We Be In Britain

It’s a question that’s been hanging over the whole financial system since the collapse in the space of a fortnight of three moderate American banks, including Silicon Valley Bank (SVB), followed by Swiss behemoth Credit Suisse.

The spectacle of regulators, political leaders and bankers spending sleepless weekends managing insolvencies, bailouts and takeovers, against the red-ink backdrop of lurching markets, has stirred bad memories of 2008 and the Great Financial Crash.

The response from Bank of England governor Andrew Bailey, repeated to MP’s on the Treasury Select Committee on Tuesday, is “don’t panic”, not yet anyway!

Mr Bailey conceded that recent events made this a moment of “heightened tension and alertness”, but that comparisons with 2008 are erroneous and, so far, UK regulations introduced post-crash are passing the test.

His diagnosis is that while the issues that brought down SVB and Credit Suisse are distinct and separate, the interconnectedness of the financial system means the risk of contagion cannot be ignored.

SVB collapsed because of poor risk management, with deposits locked into fixed incomes investments that fell in value as interest rates rose. Credit Suisse, meanwhile, after a decade of unerringly finding new scandals in which to become embroiled, finally stepped on a rake it could not recover from.

Mr Bailey found himself directly involved with the fallout from SVB, engineering the sale of its UK subsidiary to HSBC over a long weekend, with the deal only confirmed he said at 4am on the Monday, hours before markets reopened.

He also said the actions taken by the Bank proved the value of new regulation.

SVB had a distinct UK presence because its British branch had grown to the point it was required to become a separate subsidiary. That in turn gave the Bank of England and the Prudential Regulation Authority options in managing its decline, one of which was a sale.

Mr Bailey and his colleagues did concede there are lessons to learn, primarily from the speed with which confidence and, crucially, deposits were withdrawn from the banks.

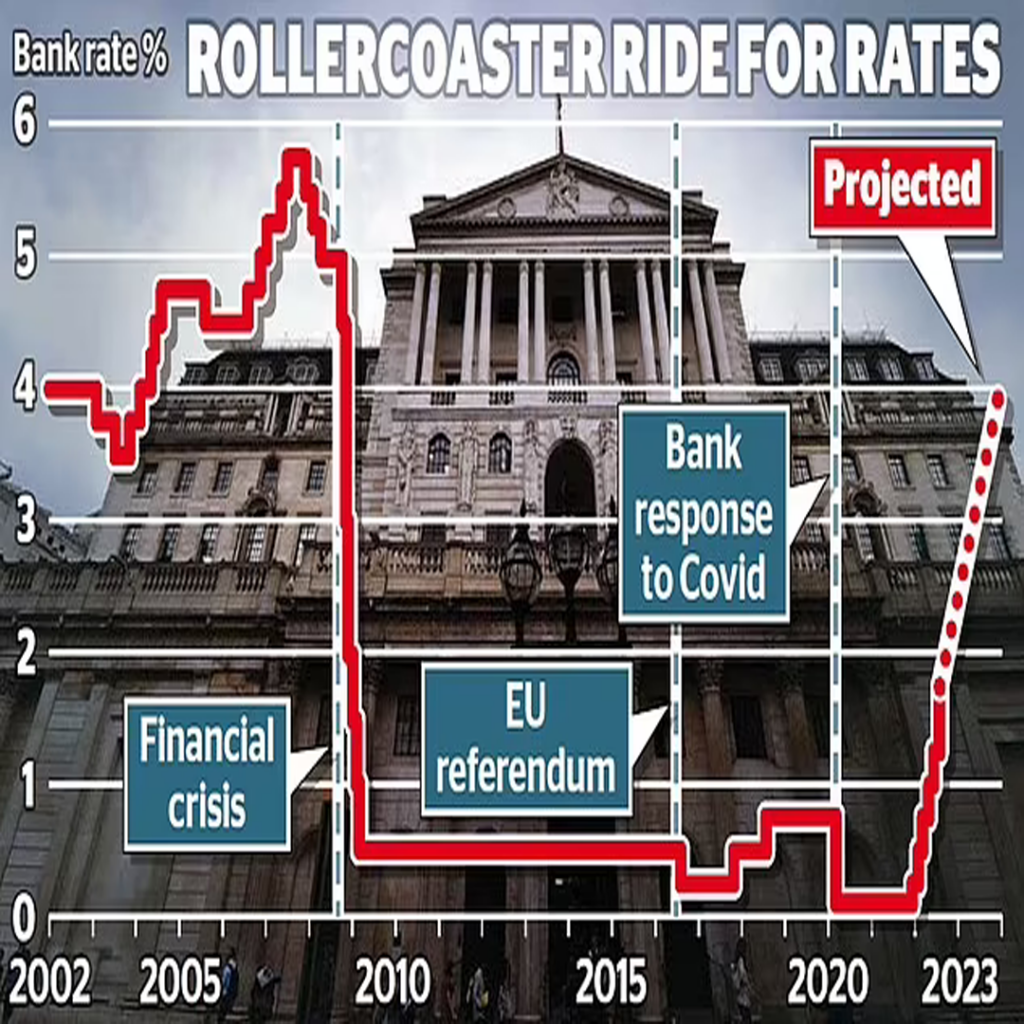

As a result, they will re-examine whether the current bank “stress tests” governing liquidity – the amount of cash banks must have on hand to absorb shocks to the system are adequate.

Technology may have helped change that calculation. In 2007 we knew Northern Rock was on the brink because customers were queuing outside branches. Today you can withdraw funds digitally in the time it takes to read this sentence, and a bank run could be underway by the end of the paragraph.

Deputy governor Dave Ramsden told MPs that messaging apps further accelerate the potential for bank runs, and said this was a factor in the SVB collapse, with the bulk of depositors all working in the tight-knit US tech industry.

“They were a tech-savvy group, already using messaging in ordinary situations, using it in a run situation.”

The result was what Bailey called “the fastest journey from health to death since Barings”, a reference to the British investment bank that collapsed spectacularly in 1995.

But he insisted the issues are bank-specific and isolated, describing the jitters that have seen banks stocks rise and fall rapidly as markets “testing” various institutions, looking for weakness. The latest example came on Friday afternoon, when Deutsche Bank’s valuation fell without an obvious trigger only to recover on Monday.

“My very strong view of the UK banking system is that it is in a very strong position,” Bailey said. “But there are moves in markets to test out firms, they are not based on identified weakness, rather they’re testing out. There’s a lot of testing going on.”

online sources: theguardian.com, news.sky.com